Value chain, industrial maturity, scaling up through practical examples: Oman and Morocco

Authors:

Stephane Aver, Chairman of HYNAT

Mahmoud Leila, Chief geologist of HYNAT

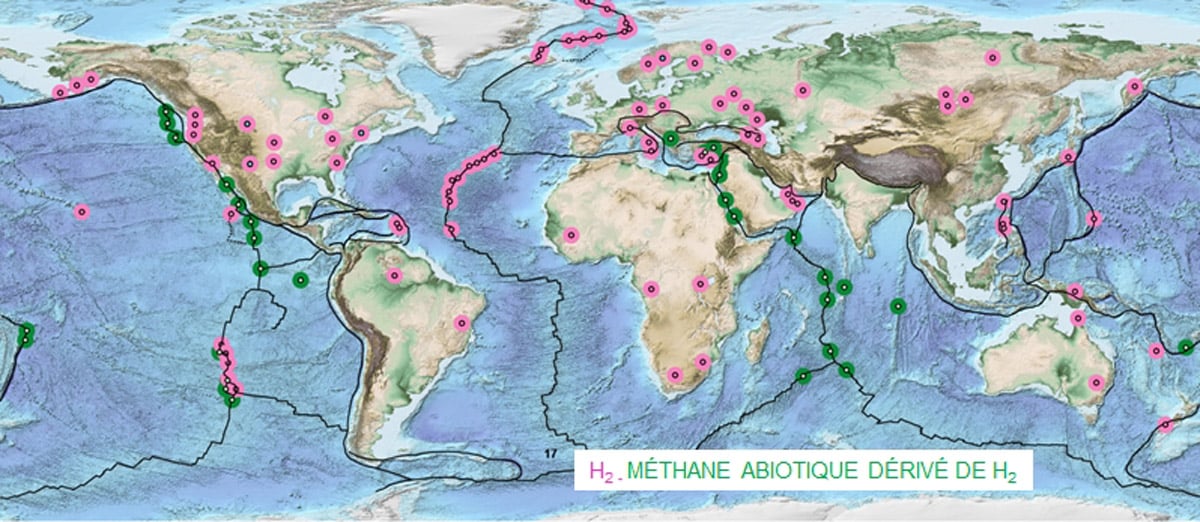

Natural hydrogen (H₂) is currently emerging from scientific curiosity to a prospective low-carbon energy commodity that can be implemented in the global energy mix, yet its readiness remains uneven across the value chain. The H2 sectoral maturity from exploration-production to market delivery needs to be evaluated through outlining the roadmap for scale-up. On the upstream end, reconnaissance detection (soil gas, micro-seepage, satellite/airborne proxies) and play-based exploration concepts have advanced to repeatable workflows; however, predictive subsurface models and resource classification frameworks are still pre-standard (pre-commercial), limiting comparability across basins. Appraisal and well engineering can borrow from oil, gas and groundwater practice, but require adaptation for H₂ (materials compatibility, embrittlement management, leak-tight completions, and intrinsically safe surface layouts).

Mapping to readiness metrics, exploration sensing and field sampling are mid-TRL (repeatable pilots), drilling/completions are mid-to-high TRL with H₂-specific gaps, while reservoir modeling, long-term monitoring (MRV), and resource reporting are low-to-mid TRL/BRL due to limited field histories. The economics hinge on discovery size, sustainable flow rates, proximity to infrastructure, and policy signals, favoring clustered developments and hybrid offtake (local + grid).

HYNAT’s activities in southern Morocco in partnership with ONHYM and the Ministry of Energy Transition and Sustainable Development since 2021—where occurrences of natural hydrogen have been verified—underscore how the presence of mature energy and logistics infrastructure (e.g., marine terminals, airports, pipelines, industrial zones…..etc.) materially enhances the value proposition of the resource. Such infrastructure reduces execution risk, shortens time-to-market, and catalyzes private investment in hydrogen-based projects, including ammonia synthesis and fertilizer production.

A similar model is being developed in the Sultanate of Oman, where HYNAT has been working with the Ministry of Energy and Minerals since one year, in collaboration with SOHAR Port and Freezone, on a programme to scale up industrial production to explore and produce natural hydrogen while consolidating the value chain through downstream conversion into ammonia and other hydrogen-derived products.

We conclude that a focused scale-up agenda should:

- establish open resource classification;

- fund multi-year pilots that couple subsurface models with production/decline data;

- qualify H₂-compatible materials and leak-integrity specs across wells and facilities;

- de-risk midstream via regulated blending pathways and modular compression/conditioning;

- create bankability enablers (of-ftake contracts, insurance, and data rooms);

- build shared geoscience datasets to accelerate play fairway mapping.

With these pillars, natural hydrogen can progress from opportunistic seeps to investable, scalable supply within an integrated low-carbon energy system.